It has been four years since I started my 401k account, and I would consider it one of the best financial decisions I have ever made. Some might say I worry too much and think too far ahead, but I disagree. The strategy is to start early. I didn’t know anything about retirement when I started my professional career back in 2014.

People kept telling me to max out my 401k contribution, and I did it without knowing the real advantages of it. Today my account has grown to over 120 thousand dollars, and I want to share with you some of the benefits I have recognized by maxing out my retirement account.

Automatic saving is the best saving strategy.

Spending is absolutely easier than saving. If I have $200 in cash, there is a high chance that I will spend it on a new pair of shoes or video games and food. It is just too much work for me to drive to the bank and deposit that money. Even after I make a deposit, it will take at least 2 to 3 days to see that money in my bank. It makes me anxious because I want to see my money immediately. Who else feels the same way?

Automatic saving, on the other hand, is painless. My employer automatically deducts contributions every time I get paid. The money goes straight to my 401k account. I don’t need to remind myself to write a check and don’t even think about it anymore after a while. My 401k enrollment form allows me to make contributions as a specific dollar amount or as a percentage of pay. When I get a raise, I give myself a raise to the plan.

Employer match = Free Money

My institution allows me to contribute up to $18,500. They will match 100% of the first 1% deferred and 50% of the next 5%. So let’s assume I earn $100,000 annually – here is how it would work: 1% would be $1000 – so I would get $1,000 as a match. Then on the NEXT 5% ($5,000), they will match it at $2,500. So the total match is $3,500. It is free money, and I would be a fool to miss out on it. At the end of the earning year, my 401k account will have a total of $22,000. We still do not count the compound interest.

Tax deduction

I get two tax breaks when I save in a 401k plan. First, my contributions are tax-deductible. The money I contribute doesn’t count toward my gross income for the year, lowering my taxable income.

When I contribute money to your 401(k), the IRS treats the contribution as a tax deduction, so I don’t owe payroll or income taxes on it. That is if I invest $18,500 through your 401(k) account and I have $100,000 in income, you are going to see an $18,500 tax deduction, lowering my adjusted gross income to $81,500.

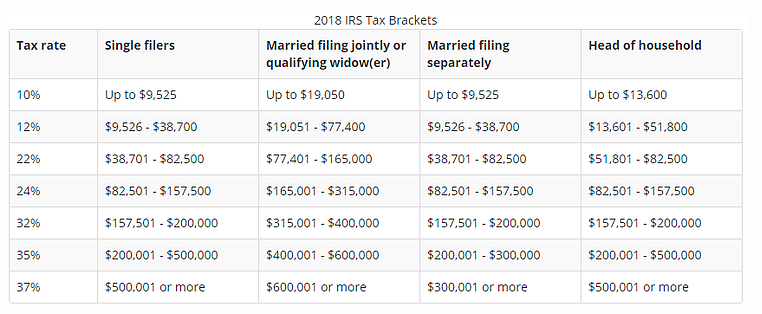

This means that 401(k) contributions have a bigger advantage as I make my way into higher income tax brackets. Let’s assume I am such an amazing worker; my boss gives me a raise, so my salary now is $160,000. If you look at the tax bracket below, I will be at the 32% tax bracket if I file as “Single.” If I want to fall into the 34% bracket, I have to contribute at least $2,500 to my 401k ($160,000 – $157,500). Of course, it is not always simple like that, but you get an idea of an average employee.

You can calculate your tax bracket here:

https://www.taxact.com/tools/tax-bracket-calculatorTheMoneyTools: 2018 Tax bracket

Increase in Your Take-Home Pay

My 401(k) plan contributions also reduce the amount of my income tax withholding. Each time I get paid, my employer withholds money for my federal income taxes based on my expected taxable income. However, if I make 401(k) plan contributions, the amount of money subject to withholding will decrease since my taxable income is less than my actual salary. The result is more money in my take-home pay each pay period.

Related: What is 401ks?

Interest compounding

This can be a difficult concept for new 401k savers to grasp, but it’s what makes a 401k plan a powerful savings tool. Put simply, my earnings are plowed back into the account so I earn interest on my original principal plus interest. Over the short term, the gains can appear small. But over the long term, you can see exponential results.

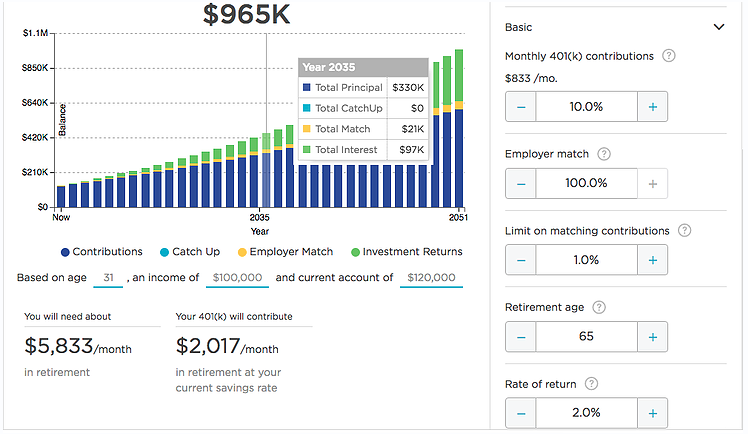

Still in doubt? How about we look at the example below:

- 31 years old right now; assume my annual salary is $100k

- My current 401k is $120k.

- If I contribute $833 every month, with a very conservative interest rate of 2% and a slight employer match of 100% for the first 1%, I will end up with $965,000 at the age of 65.

TheMoneyTools: An example of how much I will get when contributing to my 401k

Bottom Line

The main reason why I should contribute a portion of my regular income to a 401k account is to build a nest egg for retirement. However, there are many other advantages that I can get from my 401k plan, including buying a home, starting a business, or paying for emergencies. For this reason, a 401k plan is something you should start investing in today.

If you are interested in receiving more Personal Finance talks from me, consider SUBSCRIBING below.

[mc4wp_form id=”1106″]

")

{kind=link}

This sounds like a great option in saving your money and in preparing for your retirement days. I will spread this information with my loved ones. Thank you for sharing this with us.

Thanks Gervin for stopping by, hope it helps

Thanks for sharing this. I would like to know more and will search it in the net. Automatic savings is a helpful system.

I love the idea of an automatic savings system. Its just a simplified form to saving money.

I love automatic saving, especially recommend for someone who are so busy with other things going on. I don’t recommend robo advisor since there is cost associated with it. But it does worth looking into

I was not aware of this concept. Not sure whether applicable in India. Will check details

I see, I hope company in India provide some sort of retirement package

That is wonderful! It truly never hurts to plan ahead, especially when it comes to retirement.

Yes, I totally on board with saving for retirement.

I am all in if it is about saving money. Great tips and thanks for sharing the useful tips

Thank for visiting my blog

I am not familiar with the taxation in your country but in the Philippines, many realize the benefits of being updated in tax filing.

I love this topic, always gives me a little bit of sense what I need to do and be prepared for. Thanks!

love this topic! every single one of them is such an important information about taxation and how we can save money. Thanks so much for sharing

Thanks for sharing this great article . I really love to learn more about this. This kind of system would be so helpful.

[…] Related: WHY I MAX OUT MY 401Ks: $120,000 IN 4 YEARS. […]

[…] Related: Why I maxed out my 401ks […]

[…] simple answer is that I want to diversify my portfolio. I maxed out my 401k contribution every year for the past eight years. I have also put more money on the side and invested it into […]